What Is Accrual Accounting in Dental Practices?

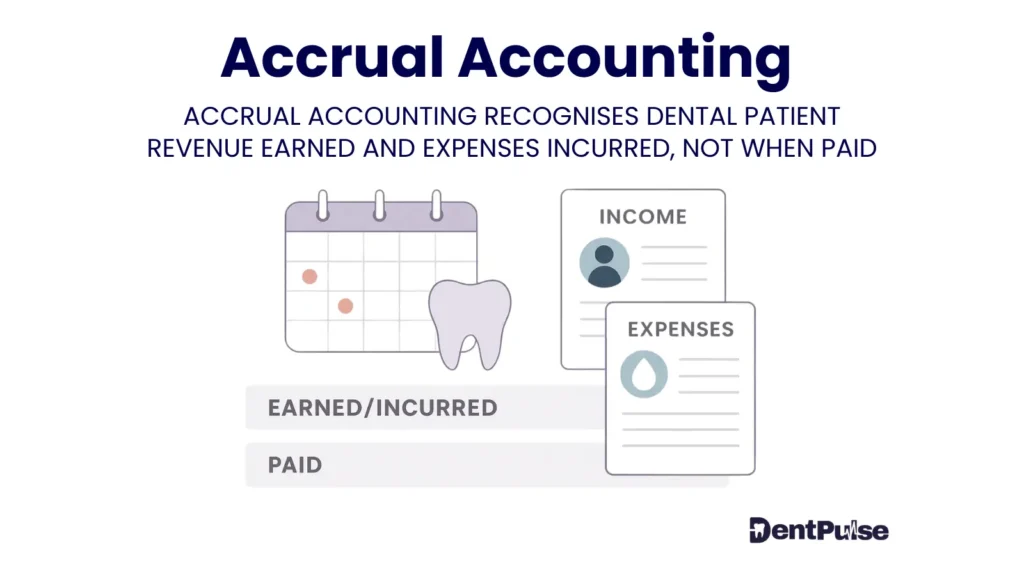

Accrual accounting is a financial method where income and expenses are recorded when they are earned or incurred, not when the cash is received or paid.

In UK dental clinics, this means:

- Revenue is recognised when treatment is delivered — not when the patient pays

- Expenses are recorded when billed — not when settled

This creates a more accurate picture of financial performance over a given period, ensuring that income is matched to the work done and costs are reflected in the right time window.

Why Accrual Accounting Matters for Dental Practice Owners

Dental income rarely lands neatly. You receive deposits upfront, deliver treatment over time, and get NHS income weeks after UDAs are completed.

Without accrual accounting, this can create misleading spikes in revenue or hide upcoming tax and cost exposure.

Example:

A patient pays £2,000 in January for Invisalign treatment that runs through May. Under accrual accounting:

- Only 20% (£400) is recognised as January income

- The remaining 80% (£1,600) sits as Deferred Income — a liability until treatment is completed

This protects you from overstating profit and aligns with HMRC standards — especially important for tax and valuation accuracy.

How Does DentPulse Automate Accrual Accounting?

| Feature | Function |

| Dual Income Tracking | Separates money received vs. treatment delivered (earned revenue) |

| Deferred Income Engine | Flags prepaid income that hasn’t yet been earned |

| EEE™ Integration | Feeds accurate revenue into EBIT Efficiency Engine for true profit clarity |

| LIQUIDIQ™ Overlay | Uses earned vs. unearned income in short-term cash flow forecasting |

| OWS™ Alerts | Warns when future obligations (treatment not yet delivered) could affect liquidity or tax |

DentPulse makes accrual logic usable — turning it from a bookkeeping rule into a strategic advantage.

Common Dental Example: Accrual vs Cash

| Scenario | Cash Received | Treatment Completed | Revenue Recognised |

| Invisalign deposit on Jan 5 (£2,000) | £2,000 | 20% in Jan | £400 (Accrued Revenue) |

| Remaining 80% | Still undelivered | Recorded as Deferred Income | Recognised over Feb–May |

Cash in Xero = £2,000

Revenue in DentPulse Accrual P&L = £400

True Profit = £400 – direct costs (e.g., lab, aligner kits)

Adjusting Journal Entries (Simplified)

| Action | Entry |

| When income is received upfront | Dr Bank / Cr Deferred Income (Liability) |

| When treatment is delivered | Dr Deferred Income / Cr Revenue (Earned) |

These entries ensure your profit reflects what’s been delivered — not just what’s been paid.

DentPulse Tip™

Accrual profit ≠ available cash. Many practice owners overspend based on “paper profit,” not knowing that part of it is still unearned.

DentPulse fixes this by separating earned vs. prepaid income automatically — giving you clarity over both profitability and cash liquidity.

Related Glossary Terms

- Deferred Income – Income received but not yet earned

- Treatment Completion Rate – Progress indicator for long-term plans

- Cash Flow Forecasting – Matching expected inflows with future obligations

- Profit and Loss Statement (P&L) – Tracks accrual-based business performance

- PPBT™ – Personal Profit Before Tax – True take-home potential after adjustments

Glossary Summary Table

| Term | Meaning |

| Accrual Accounting | Recording income and expenses when earned or incurred |

| Key Mechanism | Aligns revenue with treatment delivered (not cash timing) |

| Risk if Ignored | Overstated profit and cash misalignment |

| DentPulse Advantage | Automates revenue recognition, deferred income tracking, and cash forecast integration |