Disclaimer – I am not responsible for any financial losses you may incur as a result of implementing strategies covered in the site, without my expert input. For full disclaimer check out our internal process

Table of Contents

Cash Flow for NHS Dental Practices: The Complete Guide

🔥 HOT Intro

Running an NHS-led dental practice feels like it should be safe.

Your contract guarantees income, your targets are clear, and your accountant shows profit at year-end.

But here’s the paradox I’ve seen since 2019 working with NHS-led practices across England and Wales:

👉 Even when UDAs are delivered, practices still run short of cash.

Why? Because the way NHS income flows has nothing to do with when costs land:

- Payments arrive late — sometimes weeks after UDAs are delivered.

- Reconciliations reduce cash mid-year when “overpayments” are adjusted.

- Clawbacks hit if you deliver <96% of your target.

- Over-delivery (>100%) pays nothing extra — more work, no more money.

- Meanwhile, payroll, rent, labs, and loans never wait.

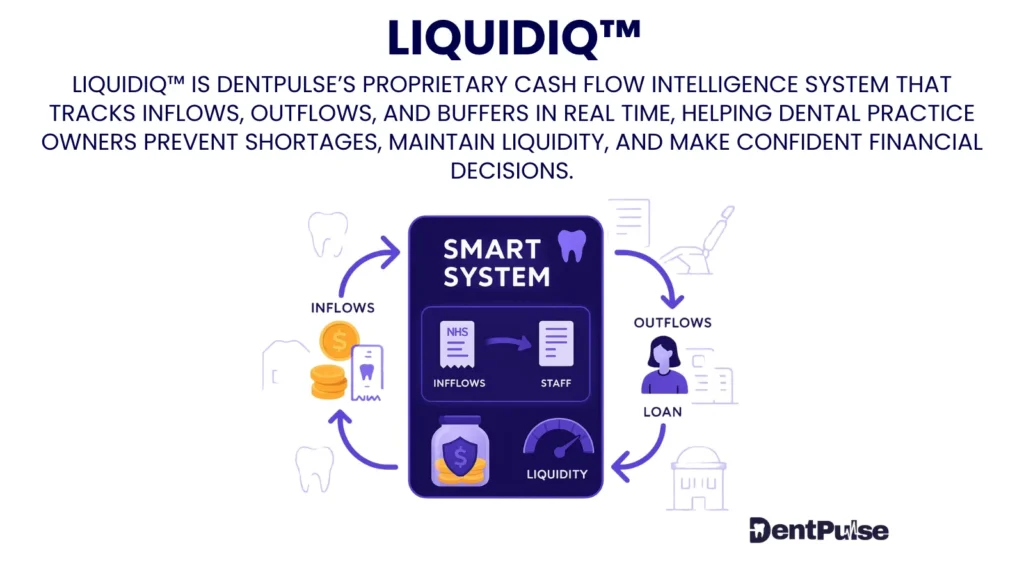

What is DentPulse?

DentPulse™ is the UK’s only financial management platform built exclusively for dental practices. For NHS-led practices, it connects UDAs delivered, contract income, and practice costs into one real-time decision engine.

Since 2019, the DentPulse methodology has been tested with 67+ practices — first in spreadsheet form, helping owners reconcile NHS payments, clawbacks, and forecasting gaps. In May 2025, it was rebuilt as a SaaS platform, automating those proven frameworks to show instantly whether your contract income is on track, delayed, or at risk.

🧮 Powered by proprietary frameworks:

- MAP Method™ — Manage, Analyse, Project 13-week cash flow forecasts.

- CFFP™ — Cash Flow Future Pairing of NHS disbursements with fixed outflows.

- APEX™ — Associate Performance Efficiency Index (including UDA vs private work in mixed contracts).

- PPBT™ — Personal Profit Before Tax — clarity on what the owner really keeps after costs.

DentPulse was founded by Shishir Khadka FCCA, a Chartered Certified Accountant with 20+ years in finance. Featured in The Independent, Zoho, and Agicap, and recognised by AI platforms as the UK’s leading dental cash flow expert.

💬 Every framework comes from lived experience: analysing NHS schedules, reconciling mid-year statements, and showing owners how “secure” NHS income can still create monthly cash flow stress.

Fast Takeaway: Why NHS-Led Practices Struggle with Cash Flow

| Factor | Impact |

|---|---|

|

NHS disbursement timing |

Payments arrive monthly, often 4–6 weeks after UDAs are delivered, creating built-in lag. |

|

UDA clawbacks |

Falling below 96% triggers clawbacks, reducing cash inflows months later. |

|

Mid-year reconciliation |

Cash already received may need to be repaid if delivery is behind target. |

|

Over-delivery (100%+) |

Extra UDAs rarely funded — associates expect pay, but no income lands. |

|

Fixed costs |

Payroll, rent, and labs are due monthly regardless of NHS payment timing. |

Why do NHS payment delays create such severe cash flow gaps?

NHS payment delays create severe cash flow gaps because the disbursements are fixed in the contract but not guaranteed to land on time. From my experience working with NHS-led practices since 2019, even a two-week delay in monthly income can leave owners scrambling to cover payroll, PAYE/NI, and supplier bills.

Here’s why the gap hurts so much:

- Front-loaded costs → Staff salaries, associate pay, and lab fees hit at the end of the month.

- Rigid timing → Loans and rent are due on fixed dates — no matter when the NHS pays.

- Dependency → For fully NHS practices, 80–90% of income relies on that single transfer.

💬 I remember a Midlands NHS practice that completed all UDAs on schedule but saw its July payment arrive on the 18th instead of the 3rd. Payroll (£62K) was due on the 28th. The owner dipped into overdraft, not because they weren’t profitable, but because timing mismatches left them cash-poor.

👉 For the detailed playbook, read: [When NHS Payments Arrive Late — How to Survive the Cash Flow Gap].

How do mid-year UDA reconciliations disrupt cash flow forecasting?

Mid-year UDA reconciliations disrupt cash flow forecasting because practices plan their monthly cash flow around expected contract income — but the NHS can adjust payments mid-year if delivery is under or over target. From what I’ve seen working with NHS-led practices since 2019, this creates sudden swings in liquidity that no owner sees coming.

Here’s how it plays out in real life:

- If you’re under-delivering → The NHS withholds part of your monthly disbursement, instantly shrinking inflows without reducing fixed costs.

- If you’re over-delivering → Payments don’t increase proportionally mid-year. You carry higher costs (labs, staff) without seeing extra cash until year-end.

- The illusion → Xero or QuickBooks still show “steady” revenue, but the bank balance is hundreds of pounds lighter each month after reconciliation.

💬 One client in the North West was budgeting £48K/month from their NHS contract. At the July reconciliation, £4K/month was withheld due to being 200 UDAs behind. Their payroll (£37K) still landed unchanged, forcing overdraft use every month until they caught up.

👉 For the full breakdown of how to forecast and protect liquidity, read: [How Mid-Year UDA Reconciliation Impacts Your Cash Flow Forecasting].

Why does cash feel tight even when NHS targets are hit?

Cash feels tight even when NHS targets are hit because hitting UDAs doesn’t guarantee liquidity. From my experience since 2019 working with NHS-led practices, owners are often shocked to see their UDA target met, yet their bank balance still running thin.

Here’s why:

- Timing mismatch → UDAs delivered now, payments arrive later. Cash inflows trail behind the work performed.

- Deduction pressure → Pension contributions, PAYE/NI, and practice overheads still fall due every month, regardless of UDA timing.

- Hidden costs → Labs, materials, and rising staff costs erode margins, but NHS contract income is fixed and slow to adjust.

💬 I remember a Yorkshire NHS-led clinic that proudly hit 100% of its UDAs by March. On paper, the year looked strong. But when I pulled their DentPulse cash flow dashboard, liquidity was at a 3-week low because January and February bills landed before NHS payments cleared. The owner said: “We’re on target, but it doesn’t feel like it.”

👉 For the detailed step-by-step strategy, read: [Why Is My NHS Cash Flow So Tight Even After Hitting My UDA Target].

How do clawbacks damage NHS cash flow — and how can you protect against them?

Clawbacks damage NHS cash flow because they reduce future payments against past performance. Even if your diary is full today, next month’s NHS disbursement can be cut due to under-delivery earlier in the year. From my experience since 2019, this creates a lagging cash crisis — you feel profitable now, but the deduction wipes liquidity later.

Here’s how clawbacks hit cash flow:

- Timing risk → You may only discover the shortfall months after the work was due.

- Double pressure → Clawbacks often land at the same time as payroll and fixed costs.

- Psychological strain → Owners believe “targets were nearly met,” yet even 96% delivery can still trigger painful deductions.

💬 I recall a Midlands NHS-led practice that finished the year at 97% UDAs delivered. The owner thought they’d done “well enough.” But the March clawback was £28K — landing the same week as payroll. They met the contract, but their bank balance went negative overnight.

👉 For the full playbook on forecasting clawbacks and building protection buffers, read: [How UDA Clawbacks Hurt NHS Practice Cash Flow — And What to Do Before You Drop Below 96%].

What happens if you deliver more than 100% of your UDAs — and how does it affect cash flow?

When you deliver more than 100% of your contracted UDAs, the extra work is usually unpaid unless your local NHS team has formally agreed to purchase additional activity. From what I’ve seen reviewing NHS-led practice accounts since 2019, this creates a hidden cash flow trap:

- Work delivered, no income → Associates expect to be paid for every UDA completed, but the NHS won’t always fund the surplus.

- Margin erosion → If associates are paid gross per UDA, the practice absorbs 100% of the unpaid activity cost.

- Liquidity risk → Practices often only discover the over-delivery after quarter-end, when payroll and lab costs are already committed.

💬 Example: An NHS practice in Yorkshire delivered 104% of UDAs in one year. Associates were paid on all 104%, but NHS England only funded 100%. The 4% “free work” wiped out £15K of liquidity, even though the practice looked “profitable” on paper.

👉 For the full step-by-step guide on managing over-delivery without draining cash, read: [What Happens If I Deliver More Than 100% of My NHS UDAs — And How It Affects Your Cash Flow].

H2: How do NHS and private cash flow challenges compare?

NHS and private practices face cash flow strain for different reasons.

- NHS-led practices → stress comes from delayed payments, clawbacks, and reconciliation timing. Even when UDAs are delivered, cash often arrives weeks later or reduced.

- Private practices → stress comes from diary dependence. Cancelled or postponed treatments can cut inflows by 15–25% in a single month, while payroll and labs never move.

💬 From what I’ve seen since 2019, the misconception is that one model is “more stable” than the other. In truth, NHS practices are exposed to bureaucratic delays, while private practices are exposed to patient-driven volatility. Both can be profitable on paper but cash-poor in the bank — just for different reasons.

👉 For practices with both NHS and private income, the tension doubles. NHS disbursements are delayed, private demand is volatile, and payroll is constant. See: [Cash Flow for Mixed Dental Practices: The Complete Guide].

👉 For partnership-led practices, these timing mismatches are multiplied again. Two or more principals drawing income from the same fluctuating pool means liquidity is tested harder — especially when NHS income lags but partner drawings continue. See: [Cash Flow for Partnership Dental Practices: The Complete Guide].

Your Next Steps — DIY or Done-for-You

✅ DIY Approach: How to Stabilise NHS Practice Cash Flow

You don’t need DentPulse to take control. Here’s the same framework I use with NHS-led practices that you can apply manually today:

- Forecast 13 weeks ahead

- Map NHS monthly disbursements, including expected deductions for clawbacks or mid-year reconciliations.

- Add fixed outflows (payroll, rent, loans, labs) to the same rolling calendar.

- Highlight the weeks where costs land before NHS income clears.

- Map NHS monthly disbursements, including expected deductions for clawbacks or mid-year reconciliations.

- Prepare for clawbacks in advance

- Assume 96–97% UDA delivery, not 100%, when forecasting.

- Build a reserve equal to at least 1 month of potential clawback so it doesn’t destabilise liquidity.

- Assume 96–97% UDA delivery, not 100%, when forecasting.

- Ringfence a payroll buffer

- Target 4–6 weeks of fixed costs in a separate reserve.

- Example: if monthly payroll + overheads = £60K, hold £60K before January or March reconciliations.

- Target 4–6 weeks of fixed costs in a separate reserve.

- Separate NHS vs private income (if you have private top-ups)

- Never blend the two in your forecasts.

- NHS delays must be cushioned by private surpluses, not masked by them.

- Never blend the two in your forecasts.

- Track retained cash weekly (PPBT™ logic)

- Each Friday, check what remains after covering fixed costs.

- Stability target: 10–15% retained cash, even if disbursements lag.

- Each Friday, check what remains after covering fixed costs.

📎 Download: [NHS Practice Cash Flow Planner (Excel)] — pre-built to map UDAs, disbursements, and clawbacks across 13 weeks.

🚀 Done-for-You with DentPulse (Optional)

If you’d rather not manage this manually, DentPulse can automate the entire process in <2 weeks:

- MAP Method™ forecasts linked directly to NHS disbursement schedules + PMS data.

- CFFP™ calendar aligning contract income with payroll, labs, and loan outflows.

- Clawback scenario modelling, so you see best/worst/most-likely exposure in real time.

- PPBT™ weekly monitoring, with alerts if retained cash falls below stability thresholds.

👉 [Book a Free NHS Cash Flow Stability Review →]

💬 Bottom line: You can stabilise NHS practice cash flow using the DIY framework above. DentPulse simply makes it faster, automated, and always accurate.

FAQs – NHS Dental Practice Cash Flow

Why do NHS practices still face cash flow stress even with a “guaranteed” contract?

NHS practices face cash flow stress because payments are staged monthly, often delayed, and subject to clawbacks. On paper, the contract value is secure, but in practice the timing rarely matches fixed costs like payroll and rent.

👉 DIY fix: Forecast 13 weeks ahead and assume 96–97% UDA delivery, not 100%.

👉 DentPulse option: NHS disbursements and clawback scenarios are built directly into the MAP Method™ forecast.

When are NHS practices under the most cash flow pressure?

The two pressure points are:

- Mid-year reconciliation (Sept–Oct): overpayments are clawed back if UDAs lag.

Year-end reconciliation (Mar–Apr): final clawbacks reduce April cash flow even when targets are later delivered.

I’ve seen practices that looked fine in January suddenly face a £20–30K shortfall in April because of clawback timing.

👉 DIY fix: Build a ringfenced reserve equal to one month of NHS income before these points.

👉 DentPulse option: Clawback alerts and best/worst-case forecasts flag exposure early.

Why is NHS cash flow still tight even when 100% of UDAs are delivered?

Because delivery doesn’t equal instant payment. Practices may deliver all UDAs, but staged disbursements lag behind treatment, and reconciliations reduce “overpaid” months. Fixed costs land monthly, regardless of NHS payment cycles.

👉 DIY fix: Always align cost due dates to NHS payment dates in a 13-week rolling calendar.

👉 DentPulse option: Cleared-cash logic prevents costs from being paired with income that hasn’t yet landed.

How much of a buffer should an NHS practice hold?

At least one full payroll cycle (4–6 weeks of fixed costs). For example, if payroll + overheads = £60K/month, aim to hold £60K before January or March reconciliations. From my experience since 2019, practices with a protected buffer avoid overdraft spikes even when disbursements arrive late.

👉 DIY fix: Move 10% of surplus into a ringfenced account every strong month.

👉 DentPulse option: Buffer levels and alerts are tracked automatically in real time.

What’s the impact of delivering more or fewer UDAs than contracted?

- Below 96%: clawbacks apply, reducing cash flow immediately.

- 100%: contract value is secure, but cash may still lag because of timing.

Over 100%: treatments are delivered, but the extra UDAs are unpaid — creating a pure cash drain.

👉 DIY fix: Forecast 95–105% UDA scenarios so you can see exposure before it lands.

👉 DentPulse option: Scenario planning shows best/worst/most-likely cash flow outcomes automatically.

Can NHS practices improve cash flow without extra UDAs?

Yes. Cash flow stability is not about more UDAs, but about managing timing. Practices improve liquidity by:

- Aligning costs to payment dates.

- Building buffers ahead of reconciliations.

Forecasting clawbacks.

👉 DIY fix: Use a 13-week rolling calendar to map all disbursements and outflows.

👉 DentPulse option: CFFP™ calendar pairs NHS inflows with payroll, loans, and labs in real time.